When One Stock Becomes a Superpower

Nvidia’s $4 trillion valuation now exceeds the GDP of the UK, France, and Canada. What that tells us about markets, and risk, today.

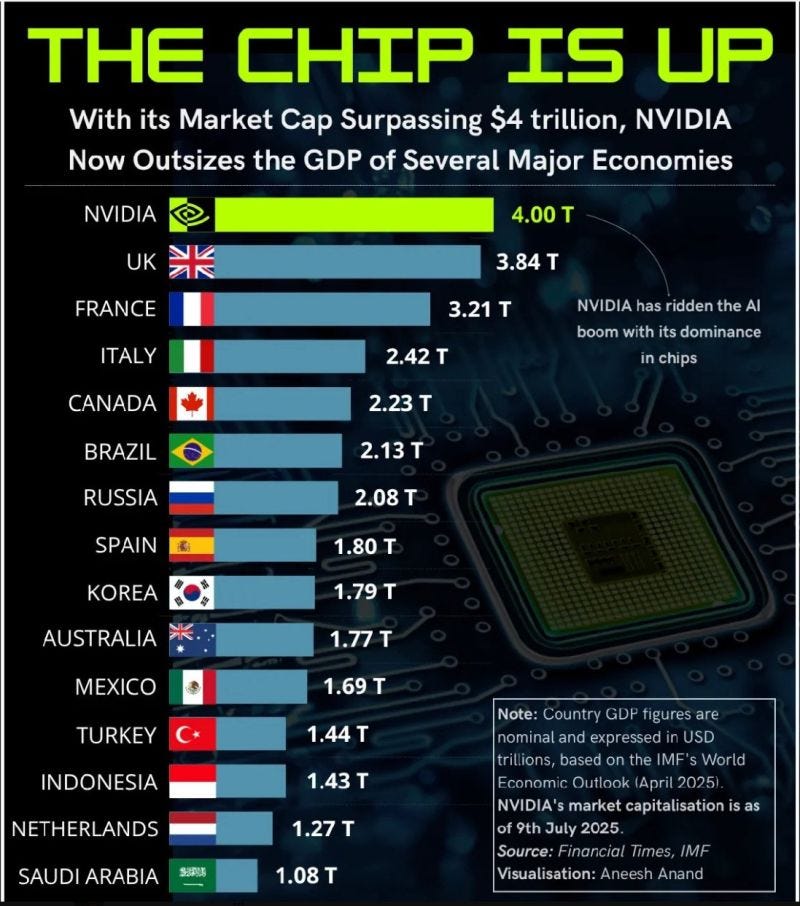

In every market cycle, there are moments that capture the psychology of the era in a single image. The chart above is one of them.

As of July 9, Nvidia's market capitalisation stands at $4 trillion, larger than the annual GDP of the United Kingdom, France, or Canada. It now exceeds the economic output of every country on earth except the United States, China, Germany, and Japan.

This is not merely a triumph of technology or earnings power. It is a reflection of where we are in the investment cycle, how investors are allocating capital, and the growing role of narratives, especially those tethered to artificial intelligence.

To be sure, Nvidia is a remarkable company. It sits at the heart of the AI value chain, dominating the market for advanced semiconductors essential to training and running large language models and AI infrastructure. But it is also a stock, subject to valuation, to cyclical forces, to investor behaviour, and the inescapable arithmetic of expectations.

We have seen this movie before. In every prior cycle, a small group of companies comes to embody the hopes of investors. From the Nifty Fifty in the early 1970s to the dot-com darlings of the late 1990s, and more recently the FAANGs, the market has often crowned a select few as “can’t miss” growth engines. And in nearly every case, the story has ended the same way: with disappointment for those who arrived late.

That Nvidia now trades at a valuation greater than most national economies is not a commentary on its intrinsic worth, but rather a statement about investor positioning. It tells us that belief in AI's transformative potential is not merely high, it is bordering on total. In market terms, this means expectations are priced for perfection.

This is not an argument against Nvidia’s long-term prospects. The company may well continue to be a major player in the ongoing AI revolution. But at current valuations, even modest disappointments—slower adoption, margin compression, geopolitical risk, could create significant downside.

From an investment standpoint, extreme valuations often reflect more than just growth assumptions. They signal emotional attachment, crowded positioning, and the type of one-way optimism that can lead to fragility. The risk is not that Nvidia fails to execute. The risk is that it does everything right and still cannot justify the valuation.

This moment also tells us something broader. When a single equity surpasses the GDP of entire G7 nations, it reflects the degree to which capital is being funnelled into a narrow set of perceived winners. It is further confirmation of the market concentration dynamic we highlighted in our recent post on the “Incredible Shrinking Stock Market.”

The AI revolution may prove every bit as transformative as the internet, but investors should not confuse technological inevitability with investment certainty. Cycles matter. Valuation matters. Positioning matters.

We continue to believe that the 2020s will be defined by regime change, both geopolitical and macroeconomic. That will translate into new leadership, new sources of return, and eventually, a rotation away from today’s market darlings.

This is not a call to short Nvidia. It is a call for balance. The most successful investors of the next decade will be those who combine discipline with flexibility, and optimism with pragmatism.

Each month in our premium service, the Global Investment Letter, I update readers on my investment activities and provide macro commentary across global equity, fixed income, currency, and commodity markets. Our focus is on helping serious investors navigate a world where fragility and opportunity now go hand in hand.

If you found this perspective helpful, I invite you to explore free sample issues of the Global Investment Letter and sign up for our complimentary weekly commentary here:

👉 www.globalinvestmentletter.com/sample-issue